Food and drink producers are facing a sustainability dilemma. The need for eco-friendly packaging is growing, but it costs more and often isn’t as versatile. Faced with anti-plastic regulation and carbon reduction targets, commitment and major investments are needed to increase renewable choices. It won’t be easy, and consumers have a role to play too

Plastic packaging is the largest single source of plastic waste in the EU

American and European consumers are using more, not less, packaging

Plastic packaging is the largest single source of plastic waste in the EU, and food and beverage packaging accounts for 40% of all of it. The question of how to shift to more sustainable packaging and how to deal with the growth in packaging waste is a mounting global issue. The fastest increase in packaging use is in Africa, Asia and Latin America, but packaging use per capita is also still rising in Europe, the US and Australia.

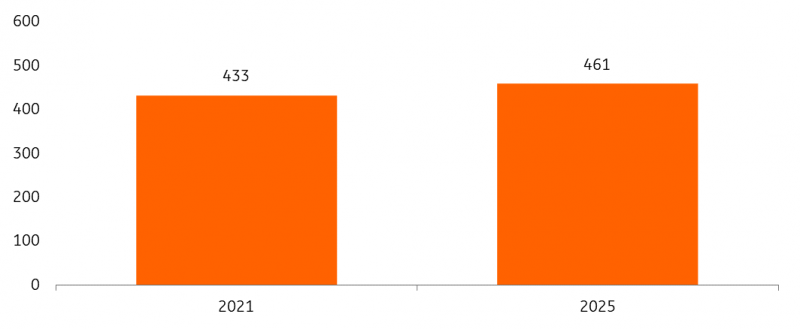

The total packaging volume for consumer goods in the US grows at about 1.5% per year, outstripping population growth. According to projections made by Euromonitor, the average American will use 1,360 units of packaging per year in 2025, up from 1,290 in 2021. In Europe, it’s expected the EU will see a 20% increase in packaging waste per capita in 2030 compared to 2018.

Packaging use in consumer goods sector in the US expected to increase by almost 30 billion units in 2025

Packaging volume, billions of units

Euromonitor, ING Research, *includes food, beverage, personal care, household products and pet food

Changes in consumption patterns are to blame

Consumer trends such as the growing demand for convenience products, such as fresh-cut fruits and meal kits, on-the-go consumption and home delivery lead to increased use of packaging material. Demographic changes contribute as well; households are getting smaller and smaller households tend to prefer smaller pack sizes. And that results in relatively more packaging material per kilogram or litre of product.

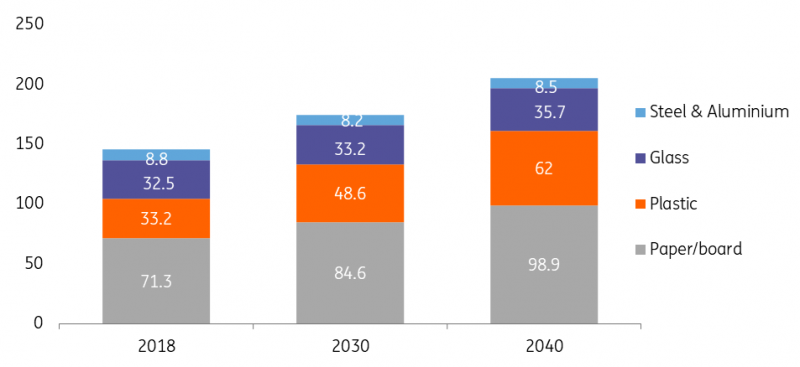

Increase in packaging waste in the EU mainly driven by plastic and paper packaging

Packaging waste in kilogram per capita

Eunomia, ING Research

It’s true that many food and beverage companies and retailers are actively seeking to reduce the size and weight of packaging, for example, through lightweight cans and bottles and by replacing rigid plastic lids with flexible plastic foils. But while such initiatives are slowing down the growth in packaging volume and waste, they don’t seem to be reversing it.

Sustainability has a price

Food and beverage packaging comes in many shapes and forms, and all have their own attributes. Functionality, marketing, and costs are all very important aspects in the decision on a certain packaging format. In the end, a food or beverage manufacturer wants packaging to keep the product safe for as long as possible, make it attractive to buy and do so at the lowest costs. There are certain trade-offs between these targets and sustainability, with sustainability often subordinate to the other criteria.

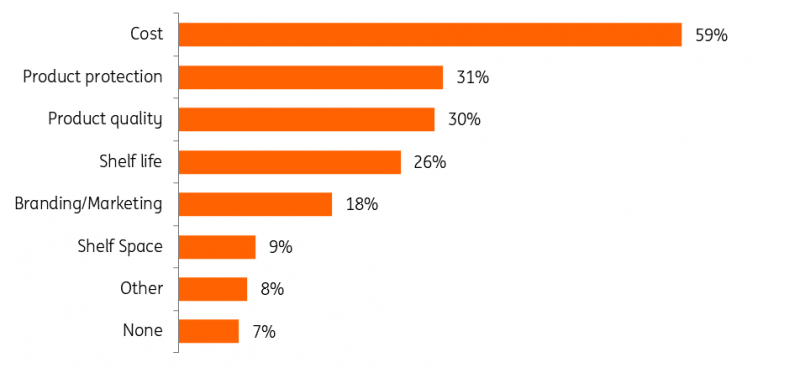

Higher costs complicate the shift to more sustainable food and beverage packaging in the US

% of respondents on the question: In adopting sustainable packaging, what trade-offs, if any, do you see most?

PMMI Packaging Compass, ING Research

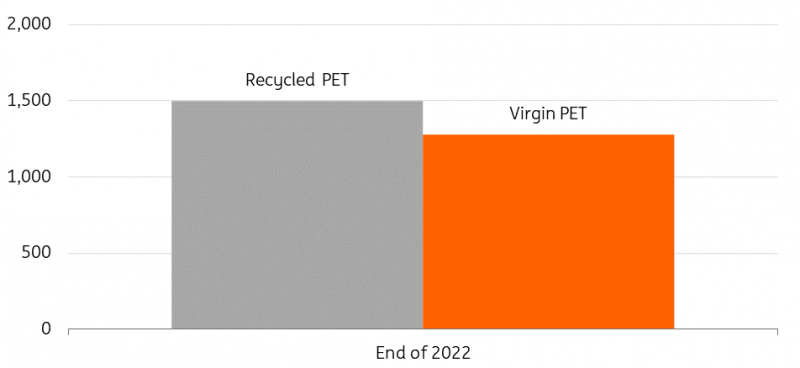

The supply of high-quality recycled material in plastics trails behind the availability of virgin material, and costs for recycled materials are often higher. In 2022 it would have cost a European beverage manufacturer around 20% more to only use recycled PET for its bottles. And if you’re wondering, PET stands for Polyethylene Terephthalate, which is a type of clear, strong, lightweight and 100% recyclable plastic.

In aluminium, it’s the other way around. Costs of used beverage cans in Europe stand at 80% of new aluminium, providing a great incentive to use recycled material to produce new cans. For aluminium, the challenge is mainly about unlocking more potential, given that national recycling rates vary widely and can be anywhere between 35 and 99%.

Recycled PET plastic trades at a premium compared to virgin material

Euro per metric tonne, free delivered Northwest Europe

S&P Global, ING Research

More demand for recycled material

Still, we do see demand growth in Europe and the US for more eco-friendly packaging materials and for packaging which is (partially) based on post-consumer recycled content. Both new legislation and the need to hit certain carbon emission reduction targets act as a catalyst for corporates. Besides, there is a clear reputational risk because packaging pollution, notably from plastic, is a major concern for consumers and NGOs (see this previous ING Research report).

Packaging a key aspect of carbon footprint of food and beverage products

Packaging is one of the more carbon-intensive parts in the lifecycle of food and beverage products due to the fossil fuel required to produce packaging materials, the fossil inputs needed to make plastics and the end-of-life treatment (recycling, incineration or landfilling) of used packaging. Calls from investors to disclose more information on the impact of plastics are getting louder. For example, check out this announcement on sustainability disclosures from the CDP environmental charity.

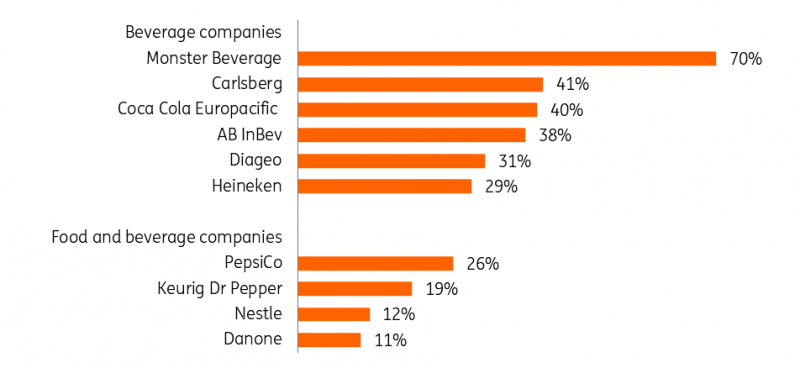

We’ve analysed 20 major food & beverage companies and find that some already report the carbon footprint of their packaging in detail. In relative terms, the share of packaging within their total footprint is largest for beer brewers and soft drinks producers. For those brewers, this mainly stems from the energy required to produce glass bottles and aluminium cans. Soft drinks producers generally have a large footprint from aluminium cans and use a large volume of plastic packaging, of which the majority doesn’t get adequately recycled.

For food manufacturers in other subsectors, such as meat, fish or bakery, we estimate that the relative share of packaging within their total emissions will generally be lower than 10%. That’s mainly because raw materials constitute a much larger share of their footprint. Still, it is considered a material topic in the sustainability strategies of almost any company in the industry.

Packaging represents a major share in the carbon footprint of food and beverage companies

Packaging related emissions as a percentage of total scope 1,2 and 3 emissions

Company information, calculations made by ING Research based on most recent reported data

Companies are signalling the potential for reducing carbon emission through packaging

For the companies we’ve analysed, the potential gains of more sustainable options are often clear. PepsiCo estimates that shifting from virgin plastic bottles to 100% recycled PET bottles reduces carbon emissions by approximately 30% per bottle. Spirits maker Diageo estimates that producing glass bottles in a biofuel-powered furnace with only recycled glass as input could lower the footprint of a regular bottle by 90%.

For companies which use a mix of materials, a shift from one material to another can also be meaningful. Beer packaging provides an example. Both plastic (PET) and returnable glass beer bottles have a carbon footprint per litre, which is about three times lower than an aluminium can and five times lower than a one-way glass bottle. But changes in the packaging material might not always be desirable from a commercial perspective.

What sort of action are food and beverage companies taking?

When food and beverage makers want to reduce the carbon footprint of their packaging, there are several actions that they can undertake.

In their own operations

- Investing in sustainable packaging design (less material, more recyclable material, better recyclability or different materials) and in the testing of new packaging formats. Common company objectives are to have 100% recyclable packaging, increase the percentage of recycled content and reduce the (relative) use of virgin material by 2025 or 2030. We’ve looked into those opportunities in this previous report on plastic packaging.

- Exploring the broader implementation of re-use schemes, which are generally most promising in beverages and food service packaging. One example is that winemakers in some European regions are working with refillable wine bottles.

- Closing the loop in their own facilities by reducing and recycling (secondary) packaging waste from production and transportation.

Upstream in the value chain

- Supporting greener packaging production technologies by partnering with packaging producers. Examples of such partnerships include glass production based on green hydrogen (for example, between glass maker Encirc and Diageo) and technologies to produce bioplastics at scale (in which chemicals companies such as Avantium collaborate with beverage firms like Coca-Cola, Refresco and Carlsberg).

- Entering into long-term off-take agreements for post-consumer recycled content with suppliers to ensure demand and facilitate investments in recycling facilities.

Downstream in the value chain

- Providing funding for community recycling services and material recovery facilities. In Europe, this is often done through extended producer responsibility schemes which oblige companies to pay for the volume of packaging that they put on the market. The proceeds can then be used to strengthen recycling systems. If such a system is not in place, support can also be done by direct investments in facilities, payments into funds or donations.

Apart from these actions, food and beverage manufacturers can also throw their weight behind legislation that encourages more comprehensive recycling systems and higher recycling rates.

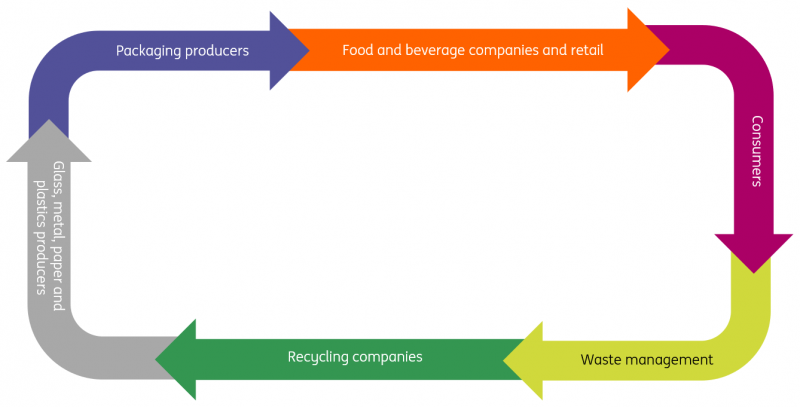

Food and beverage companies operate in a value chain with many stakeholders

Schematic depiction of the value chain for packaging

ING Research

Companies set to face more stringent regulation

Packaging regulation is getting stricter, and food and beverage companies will more often be required to pay for the packaging they put on the market, increase recycled content, improve recyclability and take steps to reduce pollution.

In practice, these laws work as a catalyst for the adoption of recycled content and improve the business case for investment in facilities where post-consumer recycled content is processed into new food-grade packaging. That capacity is urgently needed because demand for high-quality inputs such as used beverage cans and bottles exceeds supply. If domestic markets fail to keep up, imports of recycled material from elsewhere could fill the gap, leaving domestic inputs underutilised.

How is packaging legislation evolving in the EU and the US?

European Union:

At the EU level, both the introduction of the Single Use Plastics Directive (SUP) in 2019 and the current proposal for the Packaging and Packaging Waste Regulation (PPWR) shape the future of packaging. Four key elements include:

- Limits on single-use items. Both the SUP and PPWR include targets for a reduction of the packaging waste per capita, for example, by limiting the use of single-use drink cups and food containers in food service outlets.

- Recycled content. The SUP and PPWR set out minimum recycled content standards in plastic packaging for 2030 (e.g. 30 % for single-use beverage bottles), followed by a further rise towards 2040. In major EU countries, recycled content in plastic packaging is currently about 5-7%.

- Recyclable packaging. In the PPWR, there are requirements to make packaging fully recyclable by 2030 as well as proposals to ban certain packaging formats. This will limit the design options for companies.

- Deposit and return systems. Following the SUP and anticipating the PPWR, many new or extended deposit return schemes exist for plastic beverage bottles and metal beverage containers in the pipeline in countries such as the Netherlands, Poland and Romania. Meanwhile, non-EU countries such as the UK and Turkey also plan to introduce such systems. Once these schemes are in place, they will be especially beneficial for closing the loop for beverage containers.

United States:

While there is no federal legislation at hand, things are clearly moving at the state level.

- Extended producer responsibility. 2022 marked the introduction of extended producer responsibility laws in Oregon, Colorado, Maine and California. Similar laws are also being considered in more than a dozen other states.

- Recycled content. Some states (like California and New Jersey) are setting progressive targets on recycled content in several types of packaging, such as glass and plastic bottles.

Challenges are manifold

Moving to more sustainable packaging clearly provides a route to reducing emissions for food and beverage companies. But to get there, they depend on many others in the packaging value chain. Adding to the complexity is that almost every food maker also requires solutions for multiple materials to get closer to any net-zero targets. First of all, it’s about incentivising their suppliers to green their energy use and increase the share of recycled content in their packaging. Next to that, it’s about making alterations to the packaging design to use as little material as possible and to keep (national) recycling systems in mind. That means food and beverage companies also need in-depth knowledge of how their packaging formats perform in recycling.

All the while, legislation is evolving and pushing the market in a more sustainable direction. For food and beverage companies with operations in the EU, the (regulatory) landscape seems to be becoming less fragmented in the coming decade with the introduction of common recyclability and recycled content standards. Ultimately this should reduce red tape and help companies to scale up solutions.

In the US, the regulatory landscape looks set to remain very diverse. The adoption of new packaging laws creates an urgency to change packaging and packaging formats in some states but not in others.

[…] Source link […]